This tax optimization scheme is commonly used by large technology companies, particularly American ones. It generally relies on the creation of three entities:

- Two Irish companies

- A Dutch company intercalated between them

Profits are transferred from the operational Irish company to a Dutch entity, then redirected to an Irish holding company domiciled in a tax haven (for example, Bermuda or the Cayman Islands), where taxation is zero. This scheme allows for avoiding significant taxation in Ireland or other European Union member states.

Example of application by Google

- A European client purchases advertising space from Google.

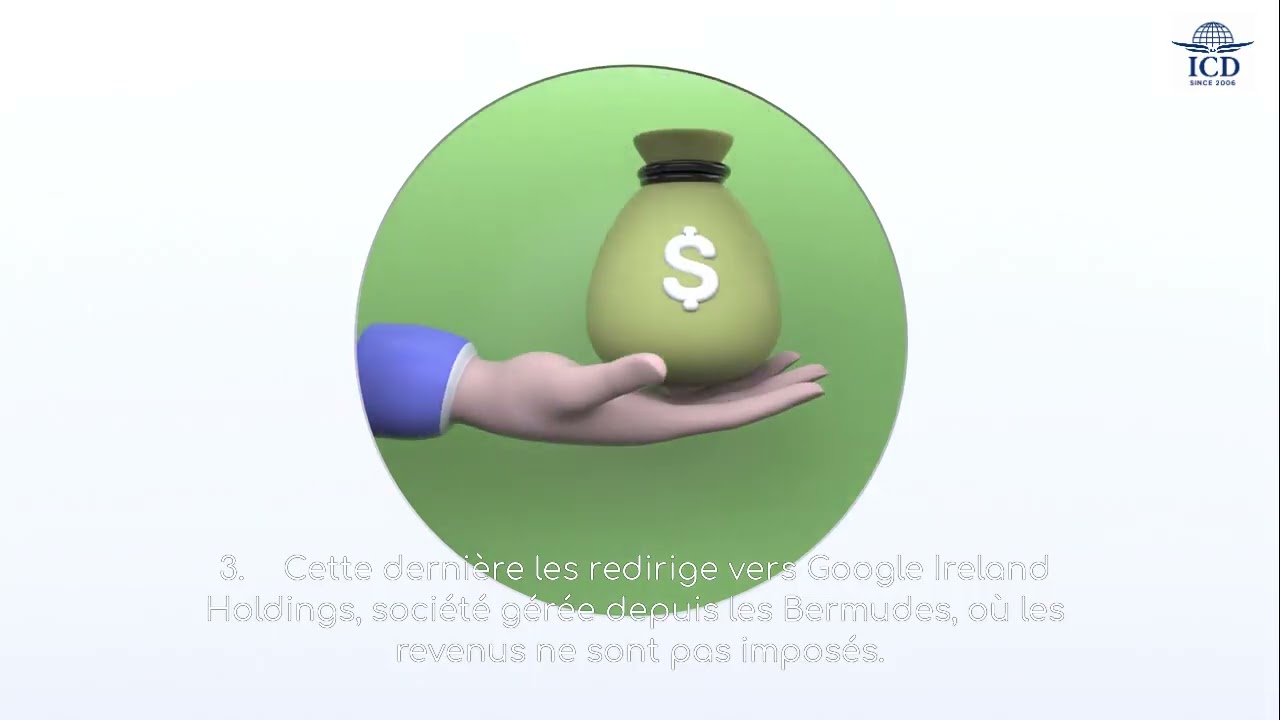

- The payment is sent to Google Ireland Ltd, which then transfers the majority of revenues to Google Netherlands B.V. in the form of royalties.

- The latter redirects them to Google Ireland Holdings, a company managed from Bermuda, where revenues are not taxed.

- Only the funds necessary for local operations remain in Ireland. This system allowed Google to channel billions of dollars while considerably reducing its tax burden.

Legal and tax foundations

This mechanism functioned thanks to several loopholes:

- Irish legislation allowed a company incorporated in Ireland to be fiscally resident abroad, under certain conditions.

- The Netherlands did not apply withholding tax on royalties paid to companies established in the EU, facilitating their transfer to zero-tax jurisdictions.

Regulatory developments

- Ireland eliminated this possibility in 2015, while allowing existing structures to persist until 2020.

- At the international level, the OECD has implemented mechanisms such as the BEPS plan (Base Erosion and Profit Shifting) and the establishment of a global minimum tax to moderate these aggressive international optimization practices.

Other companies concerned

Companies such as Apple and Amazon have also used similar structures:

- Apple used Irish companies to centralize European profits, notably resulting in a tax adjustment of 318 million euros in Italy.

- Amazon channeled its European revenues through Luxembourg and Dutch subsidiaries, thus reducing its tax burden.

Why is this subject crucial? These strategies have enabled the transfer of tens of billions of euros to reduced-taxation jurisdictions.